Physical depreciation of fixed production assets. Features of calculating the depreciation coefficient of fixed assets. Shelf life as an additional indicator of OS analysis

A feature of fixed assets and intangible assets is their multiple use. However, the time of their operation has certain boundaries; it is due to wear and tear useful application. Under wear and tear fixed assets and intangible assets should be understood as the partial or complete loss of their value and consumer properties, both during operation and during their inactivity. Distinguish between physical and moral depreciation of fixed assets.

Physical deterioration represents the loss of fixed assets of their production and technical qualities in the process of operation and the influence of natural and climatic conditions. The amount of physical depreciation of fixed assets in the process of their use is influenced by a number of factors:

the degree of loading of fixed assets in the production process;

quality of fixed assets;

features of the technological process and the degree of protection of fixed assets from the influence of external conditions;

qualification of workers and their relation to fixed assets;

quality of care of fixed assets.

Two methods are used to determine the physical depreciation of fixed assets. One is based on a comparison of the actual and standard service life or the amount of work, the other is based on data on the technical condition of the means of labor established during the survey.

The coefficient of physical depreciation (I FIZ) in terms of the amount of work can be established only for those inventory items that have a certain productivity (machines, machine tools). This coefficient can be determined by the formula:

where I FIZ - the percentage of physical wear;

T FACT - the number of years actually used by the equipment;

T NORM - standard service life (useful life);

M FACT - the average number of products actually produced per year (actual annual productivity);

M - annual production capacity (annual normative productivity).

The physical wear and tear of individual inventory objects can also be determined by their service life. This method is applicable to all types of fixed assets. Based on the assumption that physical wear and tear occurs evenly throughout the life of the means of labor, the coefficient of this wear and tear can be determined by the following formula:

.

(11)

.

(11)

According to the nature of physical wear and the period of renewal, fixed production assets are divided into the following groups:

high-strength structures - dams, dams, tunnels, etc. They are characterized by slow wear and tear and are subject to partial overhaul at long intervals;

buildings, structures, machines, in which separate parts wear out, periodically restored through major repairs;

some types of machines (cars, tractors, combines, etc.), the elements and parts of which, as they wear out, are systematically renewed and replaced with new ones (except for the main structures);

certain types of structures and transmission devices (railway and tram tracks, power grids, etc.), the renewal of which takes place continuously, through the complete replacement of all elements and parts;

apparatus, equipment and tools to be completely replaced at the end of their service life.

The physical wear and tear that occurs during the operation of an object is called physical (material) depreciation of the first kind. It is predominant and determines the amount of wear, the need for repair work and, to a large extent, the service life of the object.

However, BPF industries wear out not only during operation, but also when they are idle. Physical wear in this case occurs as a result of natural physical and chemical influences ( physical deterioration of the second kind); thus, being oxidized by atmospheric oxygen, iron and steel rust, and aluminum corrodes. The size of the losses is very significant, the annual loss of metal from rust reaches a third of the smelted volume.

The main production assets undergo not only physical, but also moral deterioration.

Obsolescence manifests itself in the loss of economic efficiency and the expediency of using fixed production assets before the expiration of the period of complete physical wear and tear. In this case, the loss of value occurs regardless of whether the main production assets participated in the production process or not.

Obsolescence is of two types. Both of them are the result of technological progress. But the economic consequences of both are different, and the need to take them into account for reimbursement purposes is not the same. The amount of obsolescence of both the first and second types is taken into account, as a rule, during the revaluation of fixed assets. Obsolescence of the first kind is to reduce the cost of machinery or equipment due to the reduction in the cost of their reproduction in modern conditions.

The relative value of obsolescence of the first type can be calculated by the formula:

(12)

(12)

where OF PERV - the initial cost of the means of labor;

OF RESTOR - the replacement cost of the means of labor.

Obsolescence of the second type due to the creation and introduction into production of more advanced and economical types of machinery and equipment.

When considering obsolescence of the second type, partial and complete wear, as well as its hidden form, are distinguished.

Partial obsolescence is a partial loss of use value and value of the machine. Gradually increasing its dimensions in individual operations can reach such values when it turns out to be appropriate to use the machine in other operations, in other production conditions, where it will still be quite effective.

Complete obsolescence- this is a complete depreciation of the machine, when its further operation in any conditions is unprofitable. It is possible that non-loss operations are still possible, but they are implemented on more productive machines. An obsolete car is dismantled for spare parts or written off as scrap metal.

Hidden form of obsolescence implies the threat of depreciation of the machine due to the fact that the task for the development of new, more productive and economical equipment has been approved.

In the traditional interpretation of obsolescence, only those changes in use value are considered that lead to a change in economic efficiency. However, the use value of tools of labor is characterized both by the quantity and quality of products produced with their help, and by the working conditions they provide. The underestimation of social factors impoverishes the content of the concepts of "use value" and "moral obsolescence" of technology.

Change social characteristics means of labor can be distinguished as a relatively independent form of movement of their use value, and the decrease in these characteristics can be defined as social wear.

The amount of social wear and tear of the means of labor is determined by the degree of discrepancy between the social characteristics of a given means or a given set of means of labor and their socially normal level.

This discrepancy may be due to two reasons:

due to the physical wear of this tool, its social characteristics have changed (for example, safety has decreased, harmful emissions have increased, the dustiness of the workplace, etc.) - social form of wear and tear,

the very level of socially normal social characteristics has changed (for example, workplace illumination standards, maximum permissible concentrations of harmful substances or other standards have become tougher) - social form of obsolescence.

The social form of both physical and moral depreciation together constitutes a single concept of social depreciation. Thus, the concept of "social depreciation of the means of labor" has a relative independence and plays a significant role in the analysis of socio-economic processes occurring during the renewal of the production apparatus.

Depending on the nature of the impact of new equipment and technology on a person (directly at the workplace or indirectly, through the environment), two types of social wear and tear can be distinguished: social and environmental. Actually social form of wear It is caused by the emergence of new technology that improves working conditions, as well as changes in the level of socially normal norms (primarily in terms of working conditions). Environmental form of wear caused by the appearance of new technology, which, to a lesser extent than the former, has negative impact on the environment, as well as the tightening of norms and restrictions on the degree and nature of the impact of production on the environment.

Varieties of the social form of wear and tear are due to the internal heterogeneity and multidimensionality of social wear and tear as a form of movement of the use value of the means of labor. The ecological form of equipment wear has a certain specificity. If the actual social form is associated with the discrepancy between working conditions and their socially normal level at a given workplace, then environmental wear and tear sometimes does not directly affect the local characteristics of jobs, but is associated with global consequences.

Environmental wear and tear, while having a certain specificity, nevertheless, has much in common with social wear and tear proper, and it can be considered within the framework of a single social form. Consideration of various types of social wear and tear leads to the conclusion that it is more economically expedient to prevent environmental pollution and create progressive working conditions in production from the very beginning than to deal with the consequences of unfavorable conditions.

In the process of functioning of fixed assets, their ultimate physical and moral wear and tear and the need to replace them with new ones come. The mechanism of transferring part of the value of fixed assets to a newly created product is called depreciation and allows, by the time of complete wear and tear, to accumulate funds for reproduction.

The concept and essence of wear

Remark 1

Wear production assets can be determined and taken into account by the building and structure, transmission device, machinery and equipment, vehicle, industrial and household equipment, etc.

Depreciation of fixed production assets is calculated for a full calendar year, regardless of the month of purchase or construction, depending on the established norms.

Depreciation cannot exceed the full (one hundred percent) cost of the fixed asset item. Accrued depreciation in the amount of 100% of the cost of an object that is suitable for further operation cannot be the reason for its write-off on the basis of complete depreciation.

Types of wear

It is customary to distinguish between 2 types of wear:

- Physical wear is a change in the mechanical, chemical, physical and other properties of material objects under the influence of production processes, forces of nature, etc. In the economic sense, physical wear is the loss of the original consumer value, the causes of which may be wear, dilapidation or obsolescence.

- Obsolescence is a loss of economic efficiency and expediency of the use of funds before the expiration of their complete physical deterioration.

The obsolescence of fixed assets can be of two types. The first type of obsolescence refers to the change in the book value of production assets when their initial cost is higher than the replacement cost.

The second type of this wear has to do with the emergence of more productive equipment.

Physical depreciation of production assets

Definition 1

Physical wear and tear can be due to several reasons: operational (associated with the production and consumption of objects), the impact of natural forces (corrosion, weathering, leaching of materials, etc.).

Physical depreciation of fixed assets is otherwise called material depreciation, characterized by the fact that during operation, fixed assets may lose their use value. This loss means the loss of useful qualities, and, consequently, the loss of its value when worn out.

The terms of physical depreciation of production assets (useful life) depend on several reasons: the degree of load, the quality of labor tools, the degree of protection from external conditions, the qualifications of maintenance personnel and other factors of influence. This type of wear can be slowed down with the help of a system of preventive maintenance, which can be capital, medium and small.

Fixed assets may be subject to capital and medium repairs, which are intended to restore their individual elements, which wear out earlier than all means of labor as a whole.

Physical wear and tear of production assets can occur not only in the course of their operation, but also in the course of their inactivity. The main production assets are subject to the degree of wear, which is a measure of the loss of their useful properties. The degree of wear can be determined by the indicator of their physical wear in accordance with the following formula:

$cf. = Tf / Tn $

Here Tf is the actual service life of production assets (in years), TN is the standard service life, which is a depreciation period.

Obsolescence of production assets

Obsolescence can be of two types:

- The first type of obsolescence consists in the loss of part of its value by means of labor due to a reduction in the cost of reproducing similar means. This type of depreciation is the difference between original and replacement cost.

- The second type of obsolescence is a decrease in the value of an object of fixed assets due to the appearance of more economical and productive machines or equipment.

There is also partial obsolescence, which is a partial loss of use value and the value of machines. If a this species wear tends to constantly increase, this may be the reason for the use of these machines in other operations in which their use will still be quite effective.

Complete obsolescence is a complete depreciation of machines, in which their subsequent use in production processes will be unprofitable.

A hidden form of obsolescence is a threat of depreciation of machines due to the approval of tasks for the development of new, more productive and economical machines. Fixed assets that are in operation for a long time are subject to both physical and moral deterioration.

AT general view the essence of obsolescence lies in the fact that fixed production assets, even before their complete physical deterioration, can become depreciated, that is, they will lose their value. The amount of obsolescence of fixed production assets can be estimated by comparing with the original and replacement cost in accordance with the formula:

$MIof = OPFperv. - OPFreset$

Here, MIof is the obsolescence of fixed production assets (in rubles), OPFperv. - the sum of the initial cost of fixed assets, OPFvost. - amount of replacement cost.

The main reason for the obsolescence of production assets is the growth of labor productivity in the industries that create these funds in the process of simultaneously reducing the cost of resources per unit of output.

Remark 2

In the case when enterprises use outdated equipment, they spend more working time, materials per unit of products they produce. At the same time, the production costs for the production of products on obsolete equipment will be significantly higher than on new equipment. If enterprises use obsolete equipment for a long time, this can lead to losses that greatly exceed the cost of this obsolete equipment.

In the production process, OPFs are subject to physical and moral wear and tear.

Physical deterioration- this is a gradual loss of physical and other properties of the BPF under the influence of labor processes or forces of nature (for example, corrosion).

The wear intensity of the BPF depends on the operating conditions, the characteristics of technological processes (P, T, the aggressiveness of the average cutting speed, the quality of equipment care, the qualifications of workers, the design of the equipment, the materials from which it is made).

Obsolescence- this is a decrease in the value of existing funds due to a decrease in the cost of reproducing similar ones (this is Obsolescence of the 1st kind).

It is unlikely to exist at present, as Fwost is constantly growing. Obsolescence of the 2nd kind consists in a decrease in the cost of OPF (machinery, equipment) as a result of the wide distribution of their more productive and economical types. The use of obsolete equipment in this way becomes inefficient and, before it is completely worn out, it must be replaced with a new one or modernized.

Example: A new apparatus has been created whose power is twice the power of the current one:

Nnew = 2000 units/year,

Nact = 1000 units/year.

The initial cost of the new apparatus is 10 million rubles, the current one is 10 million rubles, the depreciation rate is 10%.

Determine the damage from the operation of the existing apparatus

A year. action = 1 million rubles. ,

A year. new = 1.5 million rubles.

Depreciation charges per unit of production:

action = 1000000 / 1000 = 1000 rubles,

anov \u003d 1500000 / 2000 \u003d 750 rubles.

Annual damage from the operation of a morally obsolete apparatus:

Jyear. = (1000 - 750) . 1000 = 250 thousand rubles

Buildings are also subject to obsolescence. It is caused by contradictions between the requirements for buildings and their parameters, for example:

1) the inability to place new equipment in the existing building due to the insufficient height of the room for the bearing capacity of the structure of the fine grid of columns;

2) violation of sanitary and hygienic requirements. In the production of fine organic synthesis technological processes require a constant temperature and air humidity, which is impossible to organize in narrow old rooms with a large number of light openings. There are several ways to determine the degree of obsolescence of the OPF, but they are all imperfect.

1) The easiest method

and m2 = × 100 % .

2) It is also suggested to use the formula

And m2 \u003d F first. action - F perv. new .  ,

,

Where is Fperv. action, Fperv. new - the initial cost of existing and new equipment;

Wact., Wnew — annual productivity of existing and new equipment;

Tact., Tnov. — the service life of existing and new equipment.

3) Inequality proposed by V. V. Novozhilov

Zn< И¢с,

Where Зн - the reduced costs of new equipment;

I¢c - annual current production costs when working on old equipment (without depreciation).

If the inequality is met, then the equipment is considered completely obsolete and requires replacement. If not, then there is a partial obsolescence, which can be eliminated or reduced by modernization.

3) Indirectly, the obsolescence of equipment can be judged on the basis of an analysis of its age structure, according to which it is divided into the following age groups: up to 5 years, from 5 to 10 years, from 10 to 20 years and over 20 years.

The forms of compensation for depreciation are as follows.

Partial physical deterioration Reimbursed through repairs(current, medium, capital).

The enterprises plan their own expenses for carrying out all types of repairs and include them in the s/s products. In necessary cases (in order to evenly include the cost of repairs in s / s products). Businesses can create Repair Fund. For this, repair standards are developed, which are set for 5 years and are calculated according to the formula

Nrm. = . 100% ,

Where is 3 rem. - the cost of all types of repairs according to the estimate;

F ball. - the book value of the OPF.

The annual repair fund is equal to

Rgo. = Nrm. . Fbal. sg.

With complete physical and complete moral deterioration existing BPFs are replaced by new ones (capital construction, reconstruction, current replacement).

Partial obsolescence decreases or fully reimbursed by modernization, which is understood as a partial change and improvement in the design of equipment. It can be aimed at intensifying processing modes; automation; improvement of working conditions.

The source of covering the costs associated with updating and improving the BPF in the transition to market relations is the enterprise's own funds (depreciation fund and profit).

Depreciation is the loss of the physical and moral characteristics of the OPF.

Physical depreciation is the loss of the original production and technical qualities of the OPF as a result of work or inaction. Physical depreciation in percentage terms and in value terms is established by the actual, technical, condition of the object as a whole and its most important parts, assemblies or by service life.

Obsolescence - represents a premature, before the end of the physical service life, the depreciation of the OPF.

The obsolescence of the first form as a percentage is determined by revaluing the OPF, comparing their full initial cost with the replacement.

The obsolescence of the second form is established by comparing the technical characteristics of old and new OPF.

Accounting for physical and obsolescence is necessary for the correct determination of the replacement cost of funds, their service life and replacement, depreciation rates and amounts.

Depreciation is a monetary compensation for the cost of depreciation of the fixed assets, by gradually transferring their value to the products created in the production process.

The total amount of depreciation that is carried forward on manufactured products is determined as the difference between the original and salvage value of the OPF.

Depreciation is charged in accordance with the regulation on the procedure for calculating the depreciation of fixed assets and intangible assets.

Depreciation, as the process of transferring the value of fixed assets and intangible assets to the cost of products, works, services produced with their use in the course of entrepreneurial activity, includes the distribution of the cost of objects in an equivalent way between reporting periods, which together make up the useful life of each of them , the systematic inclusion of depreciation in the costs of production or circulation.

Service life - the period during which fixed assets or intangible assets retain their consumer properties.

Normative service life - established by regulatory legal acts and or by a commission organized for the implementation of depreciation policy during the period of depreciation of individual objects, fixed assets and / or selected groups of items of depreciable property.

Depreciable cost is the cost from which depreciation charges are calculated.

The annual rate of depreciation is calculated as the reciprocal of the standard service life of the facility.

When fixed assets operate in conditions that differ from those accepted, when establishing standard service lives or useful lives, it is possible to adjust the annual depreciation rate of an object or its parts by applying correction factors.

Depreciation is charged monthly. Depreciation is calculated in a linear and non-linear way.

The straight-line method consists in depreciation accrued by the organization evenly over the years over the entire standard service life or useful life of an item of fixed assets or intangible assets.

Annual rates of depreciation in the first and each of the subsequent years of the life of the facility for one owner are the same. The annual depreciation amount is determined based on the depreciable cost and the standard service life or useful life by multiplying the cost by the accepted annual linear depreciation rate.

The non-linear method consists in accruing depreciation by the organization unevenly over the useful life of an object of fixed assets or intangible assets.

With the non-linear method, the annual amount of depreciation is calculated using the sum of the number of years method or the decreasing balance method with an acceleration factor of 1 to 2.5 times. The rate of depreciation in the first and in each of the subsequent years may be different. The sum of the numbers of years of the useful life of the object is determined by the formula:

SSP \u003d C pi (C pi +1) \ 2,

where C pi is the useful life.

Under the reducing balance method, the annual amount of accrued depreciation is calculated based on the under-depreciated cost determined at the beginning of the reporting year and the depreciation rate calculated on the basis of the useful life of the object and the acceleration factor adopted by the organization.

The productive method of calculating depreciation is to calculate depreciation based on the depreciated cost of the object and the ratio of physical indicators of the volume of products produced in the current period to the resource of the object.

Depreciation examples.

1 Linear way.

Annual depreciation rate = (1 / 5) 100 = 20%.

Depreciation deductions \u003d 120 20 \ 100 \u003d 24 thousand rubles

2 Method of the sum of numbers of years.

The depreciable cost of the object is 150 thousand rubles.

During operation, OPFs are subject to wear.

Depreciation is the loss by an object of fixed assets of its consumer properties and replacement cost.

There are two types of wear: physical and moral.

Physical depreciation is the loss by the main production assets of their original qualities. Its size is influenced by factors such as the degree of equipment utilization (number of work shifts, hours of work per shift), equipment durability (service life), quality of equipment care, skill level of workers and their attitude to the BPF, etc.

Physical depreciation occurs both as a result of the use of BPF (physical depreciation of the first kind), and when they are inactive under the influence of the forces of nature (physical depreciation of the second kind).

To characterize physical wear, the wear coefficient is used, which is determined on the basis of the service life of the BPF.

If the period of actual use of the OPF (T F) is less than the useful life, then the wear factor (K F.I) is determined by the formula

where T f - the period of actual use of the BPF, year;

T p.i - useful life of the OPF, year.

If the period of actual use is longer than the useful life, the wear factor is determined in the following way:

where T B is the possible residual service life over the useful life, year.

The useful life of fixed assets is the period of time during which they generate income for the enterprise or serve to carry out the activities of the enterprise. The useful life of an item of fixed assets is determined by the organization when accepting the item for accounting.

When determining the useful life, organizations can use the "Classification of fixed assets included in depreciation groups" (Decree of the Government of the Russian Federation of 01.01.02 No. 1).

Obsolescence- this is a premature (before the expiration of the useful life) loss (decrease) in the value of the OPF.

Moral obsolescence occurs earlier than physical obsolescence and concerns mainly the active part of the BPF, i.e. machines and equipment.

There are two types of obsolescence of OPF. Depreciation of the first type means the depreciation of the OPF due to the fact that similar funds in new production and technical conditions are produced at lower costs and become cheaper. This is due to the use of the achievements of scientific and technological progress and the growth of labor productivity in the industries that produce funds. The onset of obsolescence of the first type does not entail the replacement of equipment with a cheaper one.

Obsolescence of the second type occurs as a result of the appearance of more modern, more productive equipment. Replacing old equipment with new one will lead to an increase in the volume of output and, consequently, a decrease in its cost and an increase in profits. However, the enterprise has not yet managed to recoup the used equipment, and for replacement it will have to look for additional sources of financing.

The relative value of obsolescence is determined by the formulas

where - obsolescence of the first type;

F P.S - the initial cost of the OPF, rub.;

F V.S - replacement cost, rub.

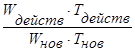

where - obsolescence of the second type;

P N (S) - the performance of the new (old) equipment.

Depreciation, both physical and moral, can be full and partial, and therefore its compensation can be complete(acquisition of new funds, capital construction, i.e. renovation of the OPF) and partial(for the physical overhaul, for moral - modernization) (Figure 4).

are functioning

OPF WEAR

PHYSICAL MORAL